Quick funding for house flipping projects throughout the Grand Strand.

Residential property flippers working the Grand Strand market have access to one of the most structurally favorable house-flipping environments on the East Coast. The combination of aging coastal housing stock, consistent inbound migration from high-COL Northeast markets, a vacation-rental investor buyer pool that pays premium prices for turnkey STR-ready properties, and a tourism economy that creates perpetual housing demand across multiple price points gives experienced Grand Strand flippers the raw material for consistent, profitable project execution. What flippers need to take full advantage of these conditions is a financing partner who can close in a week, fund renovation alongside acquisition, and actually understand what a well-renovated Garden City beach cottage or a modernized Conway historic home is worth to a retirement-market buyer or a STR investor.

Hard Money Lenders of Myrtle Beach provides residential property flippers with combined acquisition-and-renovation hard money loans that close in 5 to 7 business days, fund both purchase and rehab in a single loan structure based on after-repair value, and impose no prepayment penalties when properties sell ahead of schedule. We evaluate flip projects with Horry County market knowledge — actual comp analysis from properties in comparable condition post-renovation, not automated AVM estimates that systematically mis-price coastal properties — and we provide honest deal-analysis feedback before flippers commit to acquisitions.

The Grand Strand flip market rewards speed and precision. Properties that meet the criteria for profitable renovation — correct location, sound structure, dated-but-renovatable condition, ARV supported by genuine comparables — are acquired within days of listing. Flippers who rely on conventional financing, who underestimate the ARV complexity of coastal markets, or who don't have renovation contractors ready to mobilize at closing consistently lag behind competitors who are better-staged. We're the capital partner that stages you to compete at that level.

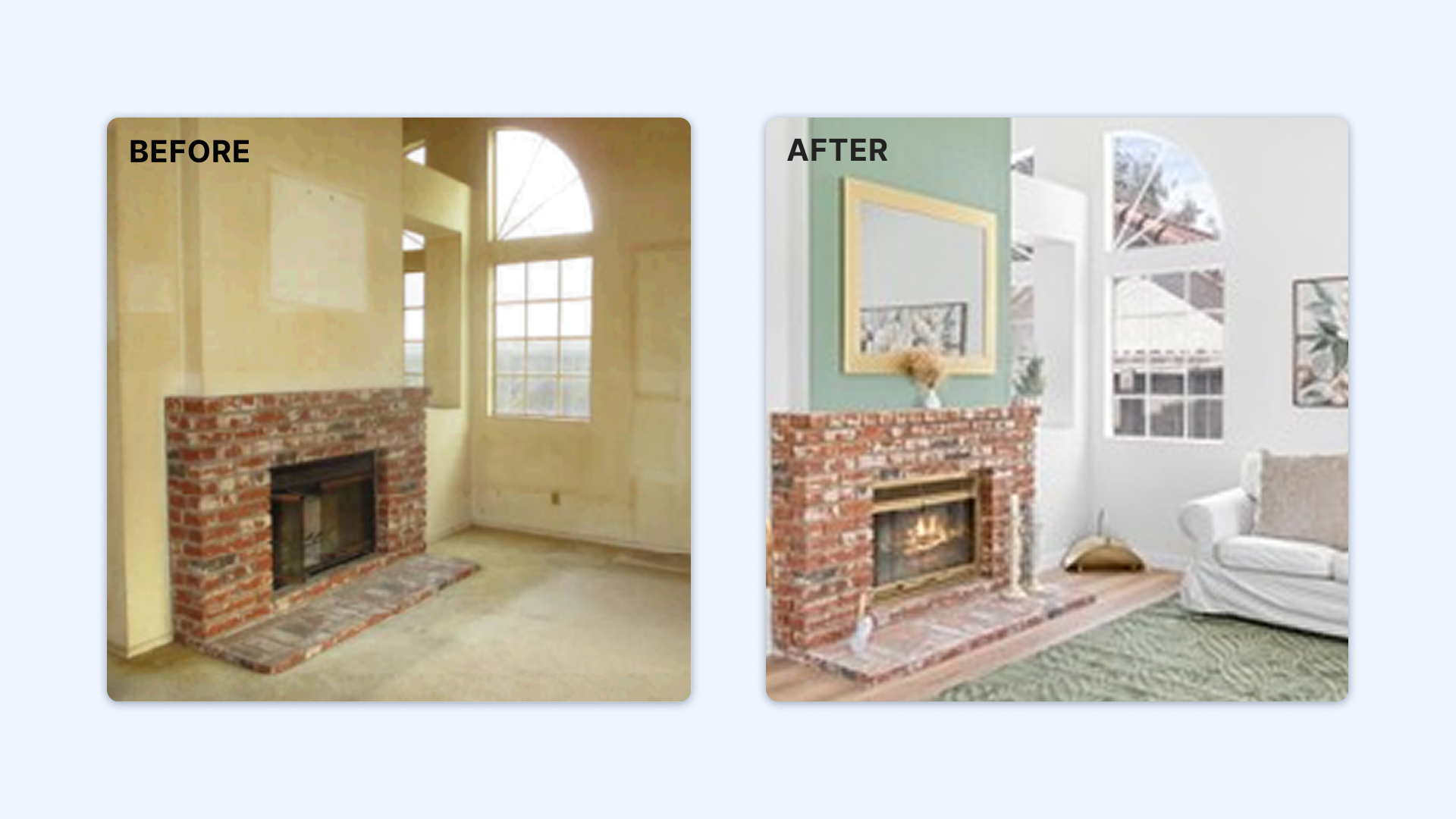

Cosmetic flips in the Conway, Socastee, and inland Myrtle Beach neighborhoods represent the most active segment of Grand Strand house flipping — properties in fundamentally sound condition where outdated kitchens, dated bathrooms, original flooring, and poor landscaping are suppressing value 15 to 25 percent below what a properly renovated home commands. These projects complete in 30 to 90 days on renovation timelines and generate net profits of $25,000 to $60,000 on acquisition prices in the $140,000 to $210,000 range. They are the appropriate starting point for new flippers and a core volume category for experienced operators building steady annual deal flow.

Structural and full-gut rehabs on higher-value properties represent the Grand Strand's most profit-rich flip opportunities. A pre-1990 beach cottage in Surfside Beach or Garden City, acquired through an estate sale at $220,000, gut-renovated with HVAC replacement, full kitchen and bath builds, wind-mitigation upgrades for insurance eligibility, and a new coastal aesthetic interior, can achieve ARVs of $380,000 to $450,000 — generating $80,000 to $100,000 in gross flip profit before holding costs. These projects require more capital, more experienced contractors familiar with coastal building codes, and more careful ARV analysis that distinguishes between STR-investor buyers (who pay income-based premiums) and owner-occupant buyers (who pay comp-based values). We analyze both buyer pools.

Post-storm and hurricane-recovery flips are a recurring Grand Strand opportunity tied to the region's Atlantic coast weather exposure. Hurricane Florence in 2018 and Dorian in 2019 both generated inventories of storm-damaged properties where sellers — particularly absentee second-home owners and estates — prioritized quick liquidation over maximum price. Investors with established financing relationships who could close within 10 days consistently acquired these properties at 25 to 40 percent discounts to post-renovation value. We maintain standing pre-approval capacity for flippers who want to be positioned for the next storm-cycle opportunity.

Vacation-rental conversion flips identify properties in STR-strong markets — Cherry Grove, Ocean Drive, and Crescent Beach in North Myrtle Beach; Garden City and Surfside Beach; Murrells Inlet — and renovate specifically to meet the expectations of vacation-rental investors who will buy finished properties as turnkey STR acquisitions. These flippers target properties in STR-permissive HOA communities, renovate to vacation-market standards (durable finishes, full-size appliances, sleeper-sofa-equipped living rooms, outdoor shower), and sell to STR operator-buyers who pay income multiples rather than pure comparable-sales values. Properly executed, these flips achieve ARV premiums of 15 to 30 percent over owner-occupant comparables.

ARV estimation is the most critical and most commonly mishandled aspect of Grand Strand house flipping. The coexistence of STR-investor buyers (paying income-based premiums in Cherry Grove and Garden City), retirement-migration owner-occupants (paying quality-and-location premiums in Carolina Forest and North Myrtle Beach's better neighborhoods), and workforce-housing buyers (price-sensitive, comp-driven in Conway and Socastee) means that the "right" ARV for a property depends heavily on which buyer pool the renovated property is actually positioned to attract. Using STR-investor comps to value a property that isn't in a STR-permissive community is a systematic overestimation error that erodes flip profits. We review ARV methodology with borrowers and correct these misalignments before they result in underfunded acquisitions.

Contractor availability and coastal renovation complexity represent the second and third challenges that claim the most flip profit. Grand Strand contractors who understand coastal building codes — wind-mitigation requirements, moisture management for salt-air exposure, FEMA-compliant flood-elevation construction — are consistently in demand, particularly during the March-through-September peak construction season. Flippers who close properties in April expecting to start renovation the following week frequently wait four to six weeks for contractor mobilization. Flippers who have established contractor relationships and close renovations in the November-through-February window execute faster, at better costs, and with fewer competitive delays.

Market-timing risk affects exit velocity. The Grand Strand real estate market peaks in spring and early summer when buyers are visiting for vacation, considering relocation, and actively purchasing. Properties that complete renovation in March and April sell faster and at better prices than properties completing in October. Flippers who can align renovation completion with peak-season buyer traffic — planning backward from a March completion date — consistently outperform those who don't manage the seasonal calendar.

Our flip-lending process starts with deal analysis. When you present an acquisition opportunity, we review the purchase price, your renovation budget and scope of work, and your ARV comparables — and we engage honestly if we see gaps. We have funded hundreds of Grand Strand flips across all price ranges and property types, and we recognize overestimated ARVs, underestimated renovation costs, and geographic-submarket mismatches immediately. Our feedback before you're under contract has saved borrowers from bad deals and kept their flip operations profitable over multiple projects.

Once you're under contract, our loan process moves quickly. Pre-approval within 24 hours, property inspection and title review within 48 to 72 hours, and closing within 5 to 7 business days. Renovation draws are processed within two to three business days of inspection — fast enough to maintain contractor payment schedules without cash-flow gaps that delay project timelines. We're available throughout the renovation period for deal-specific questions about pricing, contractor management, or exit-timing strategy.

We fund fix-and-flip projects throughout the Grand Strand flipping market including Myrtle Beach, North Myrtle Beach (Cherry Grove, Ocean Drive, Crescent Beach, Windy Hill), Surfside Beach, Garden City, Murrells Inlet, Conway (historic district and surrounding neighborhoods), Carolina Forest, Socastee, and all Horry and Georgetown County neighborhoods.

Most fix-and-flip loans close within 5 to 7 business days from completed application and executed purchase contract. For time-sensitive situations — estate sales with executor deadlines, REO properties with bank-set close requirements, or competitive multiple-offer situations — we can occasionally close in 3 to 5 days when title is clean and documentation is complete. Our pre-approval letters are available within 24 hours of application to support offer submission in competitive situations.

Yes. Our fix-and-flip loans include funding for both property acquisition and renovation costs in a single loan. We typically lend up to 70 percent of after-repair value (ARV), which for well-structured deals often covers 85 to 100 percent of the acquisition price plus 100 percent of renovation costs. The renovation portion is held in escrow and released in draws as work is completed and inspected. No separate renovation loans or personal credit cards required.

For properties in STR-active markets like Cherry Grove, Ocean Drive, and Crescent Beach in North Myrtle Beach, we evaluate ARV using both comparable sales to recent STR-investor buyers and income-capitalization analysis based on prevailing STR revenue for comparable units. In strong STR markets, investor buyers pay premiums over owner-occupant comparables because rental income supports higher pricing. We use the ARV approach that most accurately reflects the likely buyer pool — which requires understanding whether the specific property and HOA permit STR use.

We recommend budgeting a 15 to 20 percent renovation contingency for Grand Strand properties, particularly those with coastal exposure, pre-1995 construction, or known moisture-related risk factors. If your renovation exceeds budget within the contingency range, contingency reserves fund the overage. For larger overruns, we evaluate modification options including additional borrower equity contribution, scope adjustment, or loan modification if the revised ARV still supports increased loan proceeds. Open communication at the first sign of a budget problem gives us the most options — surprises at project completion give us the fewest.

No. Our fix-and-flip loans have no prepayment penalties. If your property sells in month three of a six-month loan term, you owe interest only through the payoff date — there are no minimum-interest requirements or early-exit fees. Fast execution is how Grand Strand flippers make money, and our loan structure rewards it rather than penalizing it.

Get started today and receive multiple competitive loan offers from verified hard money lenders who understand your unique needs.